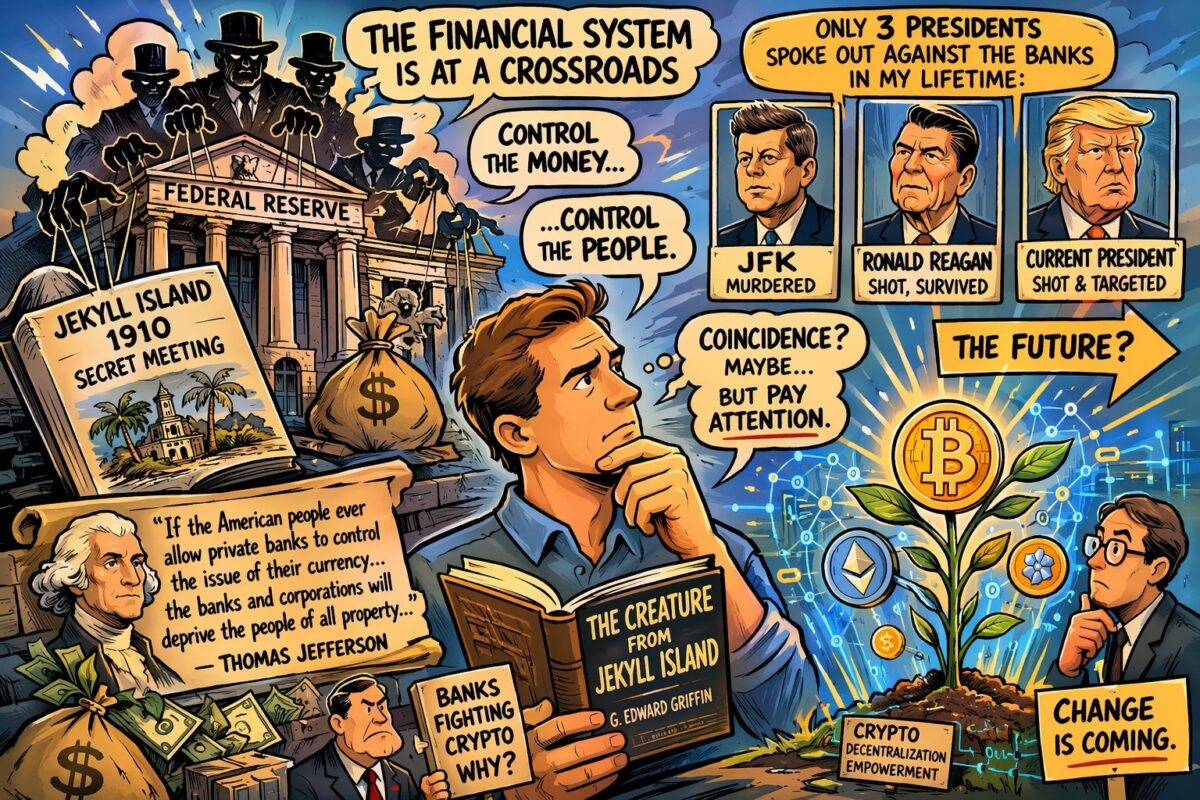

CONTROL THE MONEY, CONTROL THE PEOPLE

I’ve spent a lot of time thinking about the direction of our financial system here in the United States, and I can’t shake the feeling that we’re on the edge of some major changes, changes that, frankly, might be long overdue. Maybe I’m wrong, but when you start connecting certain dots, it makes you pause. For example, in my lifetime, only a handful of presidents have openly criticized the banking system. John F. Kennedy was assassinated under circumstances that still fuel debate decades later. Ronald Reagan survived an assassination attempt. And our current president has also faced serious threats to his life. Is there a connection? Probably a coincidence, but it’s the kind of coincidence that makes people pay attention.

One thing I keep coming back to is the rise of cryptocurrency. Whether you believe in it or not, it’s hard to ignore. It represents something fundamentally different from the traditional banking system, and the fact that large financial institutions have spent significant resources trying to regulate or push back against it says a lot. To me, that signals disruption, and disruption often leads to transformation.

A lot of these thoughts were reinforced when I revisited The Creature from Jekyll Island by G. Edward Griffin. The book takes a deep dive into the origins of the Federal Reserve and paints a picture that’s hard to ignore. Griffin walks readers back to 1910, to a private meeting on Jekyll Island, Georgia. This wasn’t just any meeting. It included some of the most powerful bankers and industrialists of the time, people tied to names like Morgan and Rockefeller. According to Griffin, they met in secret to design what would eventually become the Federal Reserve System.

The secrecy alone raises eyebrows. Participants reportedly used aliases and took steps to ensure the public wouldn’t know what was being discussed. Griffin argues that this wasn’t about protecting the economy, it was about consolidating control. At the time, the country had experienced financial instability, especially during events like the Panic of 1907. That instability created fear, and fear created an opportunity. The idea of a central bank was presented as a solution, but Griffin suggests it was also a way for a small group to gain significant influence over the nation’s money supply.

One of the book’s core arguments is that the Federal Reserve doesn’t operate the way most people think it does. Rather than being purely a government entity, Griffin claims it functions more like a private system with deep ties to major banks. That structure, he argues, allows for practices like creating money through debt, essentially lending more than is actually held. While that might sound abstract, the real-world impact shows up in cycles of economic booms followed by painful busts, something many Americans have experienced firsthand.

Griffin goes even further, suggesting that this system benefits those at the top while leaving everyday people to deal with the consequences. He connects the dots between monetary policy, inflation, and financial crises, arguing that these aren’t random events but outcomes of a system designed with certain priorities in mind. Whether you agree with him or not, it’s a perspective that challenges the mainstream narrative.

He also raises constitutional questions, pointing out that the Founding Fathers intended for the government, not private institutions, to control the nation’s currency. That idea ties back to a powerful warning from Thomas Jefferson, who once said that private banks controlling currency could ultimately strip wealth from the people. Jefferson believed that the power to issue money should belong to the public, not financial institutions, and his words feel surprisingly relevant today. I’m not convinced that the government is a better option.

What stands out most to me isn’t just the history. It’s the pattern. We’ve seen financial crises ripple through our economy time and time again, and each one seems to raise the same questions about transparency, accountability, and control. At the same time, new technologies like cryptocurrency are challenging the status quo in ways we’ve never seen before.

I’m not claiming to have all the answers. But I do think it’s worth paying attention. Whether it’s the structure of the Federal Reserve, the rise of digital currencies, or the broader role of banks in our economy, these aren’t small issues. They affect everything, from the value of your savings to the stability of the entire system. And as I get closer and closer to retirement, I would like to have something left after nearly 60 years of labor.

At the very least, being informed matters. Because if history has taught us anything, it’s that systems don’t change until people start asking questions.